Scalar-on-Function Regression

Source:vignettes/articles/scalar-on-function.Rmd

scalar-on-function.RmdIntroduction

Scalar-on-function regression predicts a scalar response from a functional predictor . This is the most common regression setting in functional data analysis: you have curves and want to predict a number.

Which Method Should I Use?

| Method | Function | Key parameter | Best when |

|---|---|---|---|

| FPC Regression | fregre.lm() |

(# components) | Default choice; full diagnostics/explainability |

| PC Regression | fregre.pc() |

(# components) | Pure R alternative to fregre.lm()

|

| Basis Expansion | fregre.basis() |

(penalty) | Smooth , interpretable coefficient |

| Nonparametric | fregre.np() |

(bandwidth) or | Nonlinear relationships |

| Elastic | elastic.regression() |

, warps | Phase-variable curves |

Quick decision rule:

- Start with

fregre.lm()— it has the richest downstream support (explainability, diagnostics, uncertainty quantification). - Test linearity with

flm.test(). If rejected, tryfregre.np(). - If curves are misaligned, consider

elastic.regression()(seevignette("articles/elastic-regression")).

The Functional Linear Model

The foundational model in scalar-on-function regression is:

where:

- is the scalar response for observation

- is the functional predictor observed over domain

- is the intercept

- is the coefficient function (unknown, to be estimated)

- are i.i.d. errors

The coefficient function describes how the predictor curve at time influences the response. A positive means higher predictor values at time increase .

The Estimation Challenge

Unlike classical regression where we estimate a finite number of parameters, here we must estimate an entire function . This is an ill-posed inverse problem:

Ill-posedness. The integral operator is compact, so infinitely many solutions may exist and the least-squares estimate is wildly unstable.

Curse of dimensionality. Discretizing at grid points gives parameters from observations. When , the model is massively overparameterized.

fdars provides four approaches to regularize this problem, each described in the sections below.

FPC Regression (fregre.lm)

fregre.lm() estimates

by projecting onto functional principal components

(FPCs). This is the recommended default: it has the Rust backend,

supports standard errors and GCV, and is the only model with full explainability, diagnostics, and uncertainty quantification

support.

Mathematical Formulation

Let be the eigenfunctions of the covariance operator of , and let be the FPC scores. Expanding and substituting gives:

This reduces the functional regression to an ordinary multiple regression on FPC scores. The coefficient function is recovered as:

The number of components controls the bias–variance trade-off: too few components oversimplify ; too many introduce noise.

Standard Errors and GCV

With the FPC scores as predictors, standard OLS inference applies. The variance of is where is the score matrix. Generalized cross-validation provides a computationally efficient alternative to leave-one-out CV:

where are the diagonal elements of the hat matrix .

Basic Usage

set.seed(42)

n_lm <- 80

m_lm <- 100

t_lm <- seq(0, 1, length.out = m_lm)

# Simulate functional predictor

X_lm <- matrix(0, n_lm, m_lm)

for (i in 1:n_lm) {

X_lm[i, ] <- sin(2 * pi * t_lm) * runif(1, 0.5, 2) +

cos(4 * pi * t_lm) * rnorm(1, sd = 0.3) +

rnorm(m_lm, sd = 0.1)

}

beta_true_lm <- sin(2 * pi * t_lm)

y_lm <- X_lm %*% beta_true_lm / m_lm + rnorm(n_lm, sd = 0.3)

fd_lm <- fdata(X_lm, argvals = t_lm)

fit_lm <- fregre.lm(fd_lm, y_lm, ncomp = 3)

print(fit_lm)

#> Functional Linear Model (FPC-based)

#> ====================================

#> Number of observations: 80

#> Number of FPC components: 3

#> R-squared: 0.435

#> Adjusted R-squared: 0.4127

#> GCV: 0.097Cross-Validation for Component Selection

fregre.lm.cv() selects the optimal number of FPC

components via k-fold cross-validation.

cv_lm <- fregre.lm.cv(fd_lm, y_lm, k.range = 1:8, nfold = 10)

cat("Optimal ncomp:", cv_lm$optimal.k, "\n")

#> Optimal ncomp: 3

cat("CV errors:", round(cv_lm$cv.errors, 4), "\n")

#> CV errors: 0.0974 0.0965 0.0965 0.0977 0.0982 0.0984 0.098 0.1001PC Regression (fregre.pc)

fregre.pc() uses the same FPC-based approach as

fregre.lm() but is implemented in pure R. It is

mathematically equivalent — choose fregre.lm() when you

need the downstream explainability/diagnostics ecosystem; choose

fregre.pc() if you prefer a pure-R solution.

Mathematical Formulation

Using FPCA, each curve is represented as:

Truncating at components and substituting into the functional linear model:

The coefficient function is reconstructed as:

Cross-Validation for Component Selection

# Find optimal number of components

cv_pc <- fregre.pc.cv(fd, y, ncomp.range = 1:10, seed = 42)

cat("Optimal number of components:", cv_pc$optimal.ncomp, "\n")

#> Optimal number of components: 1

cat("CV error by component:\n")

#> CV error by component:

print(round(cv_pc$cv.errors, 4))

#> 1 2 3 4 5 6 7 8 9 10

#> 0.2662 0.2670 0.2724 0.2722 0.2740 0.2688 0.2778 0.2714 0.2747 0.2722Prediction

# Split data

train_idx <- 1:80

test_idx <- 81:100

fd_train <- fd[train_idx, ]

fd_test <- fd[test_idx, ]

y_train <- y[train_idx]

y_test <- y[test_idx]

# Fit on training data

fit_train <- fregre.pc(fd_train, y_train, ncomp = 3)

# Predict on test data

y_pred <- predict(fit_train, fd_test)

# Evaluate

cat("Test RMSE:", round(pred.RMSE(y_test, y_pred), 3), "\n")

#> Test RMSE: 0.457

cat("Test R2:", round(pred.R2(y_test, y_pred), 3), "\n")

#> Test R2: 0.219Basis Expansion Regression (fregre.basis)

Basis expansion regression represents both the functional predictor and the coefficient function using a finite set of basis functions, providing a different regularization strategy.

Mathematical Formulation

Let be a set of basis functions (e.g., B-splines or Fourier). We expand:

Substituting into the functional linear model:

where is the inner product matrix with entries .

Ridge Regularization

To prevent overfitting, we add a roughness penalty:

The penalty discourages rapid oscillations.

Basis Choice

- B-splines: Flexible, local support, good for non-periodic data

- Fourier: Natural for periodic data, global support

Basic Usage

# Fit basis regression with 15 B-spline basis functions

fit_basis <- fregre.basis(fd, y, nbasis = 15, type = "bspline")

print(fit_basis)

#> Functional regression model

#> Number of observations: 100

#> R-squared: 0.5805754Regularization

# Higher lambda = more regularization

fit_basis_reg <- fregre.basis(fd, y, nbasis = 15, type = "bspline", lambda = 1)Cross-Validation for Lambda

# Find optimal lambda

cv_basis <- fregre.basis.cv(fd, y, nbasis = 15, type = "bspline",

lambda.range = c(0.001, 0.01, 0.1, 1, 10))

cat("Optimal lambda:", cv_basis$optimal.lambda, "\n")

#> Optimal lambda: 10

cat("CV error by lambda:\n")

#> CV error by lambda:

print(round(cv_basis$cv.errors, 4))

#> 0.001 0.01 0.1 1 10

#> 0.6124 0.5766 0.4332 0.3047 0.2794Fourier Basis

For periodic data, use Fourier basis:

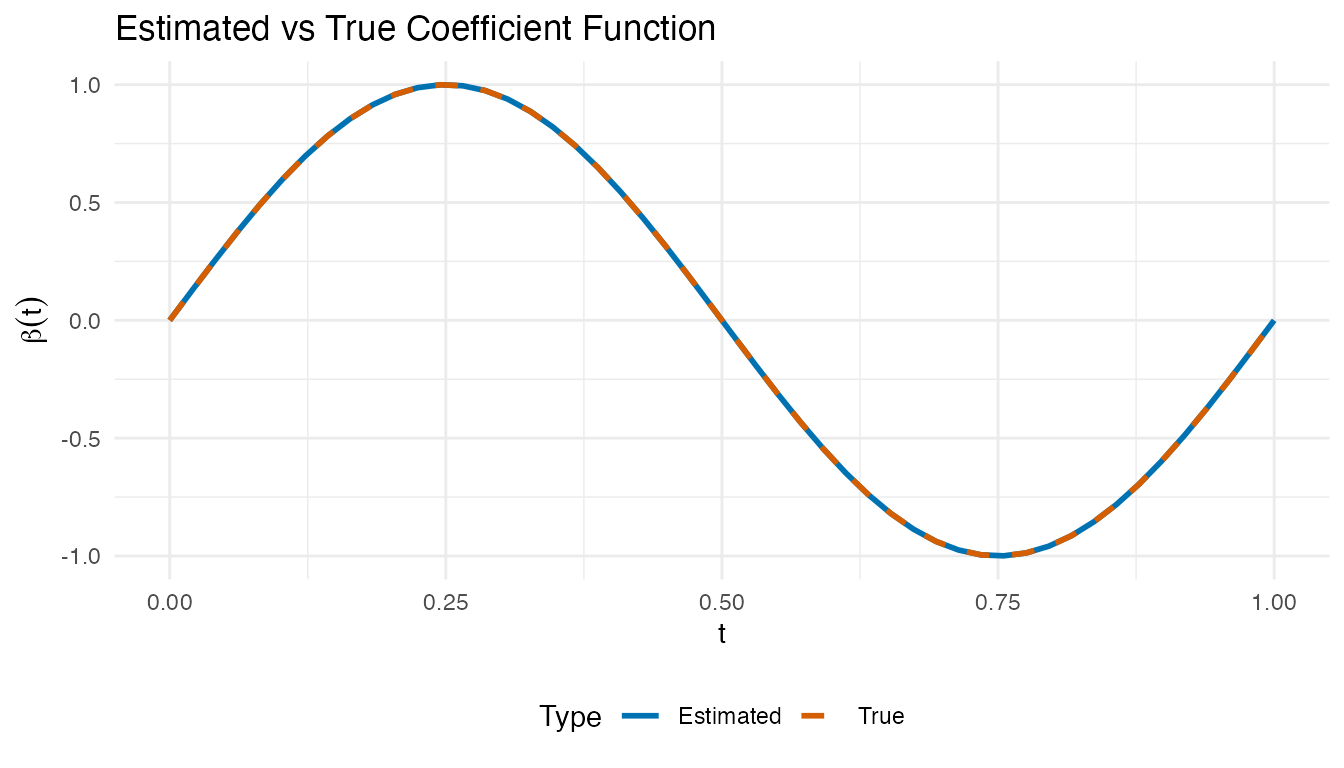

fit_fourier <- fregre.basis(fd, y, nbasis = 11, type = "fourier")Visualizing the Estimated Beta(t)

The coefficient function reveals which time points drive the response. Positive regions mean higher predictor values there increase ; negative regions decrease it.

# Reconstruct beta_hat(t) from basis regression coefficients

beta_hat <- fit_basis$beta.est

# Compare estimated vs true beta(t)

df_beta <- data.frame(

t = rep(t_grid, 2),

beta = c(beta_hat, beta_true),

Type = rep(c("Estimated", "True"), each = m)

)

ggplot(df_beta, aes(x = t, y = beta, color = Type, linetype = Type)) +

geom_line(linewidth = 1) +

scale_color_manual(values = c("Estimated" = "#0072B2", "True" = "#D55E00")) +

scale_linetype_manual(values = c("Estimated" = "solid", "True" = "dashed")) +

labs(title = "Estimated vs True Coefficient Function",

x = "t", y = expression(beta(t))) +

theme(legend.position = "bottom")

Nonparametric Regression (fregre.np)

Nonparametric functional regression makes no parametric assumptions about the relationship between and . Instead, it estimates directly using local averaging techniques.

The General Framework

Given a new functional observation , the predicted response is:

where are weights that depend on the “distance” between and the training curves .

Nadaraya-Watson Estimator

The Nadaraya-Watson (kernel regression) estimator uses:

where is a kernel function and is the bandwidth.

| Kernel | Formula |

|---|---|

| Gaussian | |

| Epanechnikov | |

| Uniform |

k-Nearest Neighbors

The k-NN estimator averages the responses of the closest curves:

Two variants are available:

-

Global k-NN (

kNN.gCV): single selected by leave-one-out CV -

Local k-NN (

kNN.lCV): adaptive that may vary per prediction point

Bandwidth Selection

# Cross-validation for bandwidth

cv_np <- fregre.np.cv(fd, y, h.range = seq(0.1, 1, by = 0.1))

cat("Optimal bandwidth:", cv_np$optimal.h, "\n")

#> Optimal bandwidth: 0.2Different Kernels

# Epanechnikov kernel

fit_epa <- fregre.np(fd, y, Ker = "epa")

# Available kernels: "norm", "epa", "tri", "quar", "cos", "unif"Multiple Functional Predictors

When the response depends on more than one functional predictor,

fregre.np.multi() extends nonparametric regression to

handle a list of functional predictors.

# Simulate a second functional predictor

set.seed(123)

X2 <- matrix(0, n, m)

for (i in 1:n) {

X2[i, ] <- cos(2 * pi * t_grid) * rnorm(1, 0, 0.5) +

rnorm(m, sd = 0.1)

}

fd2 <- fdata(X2, argvals = t_grid)

# Response depends on both predictors

beta_true2 <- cos(4 * pi * t_grid)

y_multi <- numeric(n)

for (i in 1:n) {

y_multi[i] <- sum(beta_true * X[i, ]) / m +

0.5 * sum(beta_true2 * X2[i, ]) / m +

rnorm(1, sd = 0.3)

}

# Fit with multiple functional predictors

fit_multi <- fregre.np.multi(list(fd, fd2), y_multi)

print(fit_multi)

#> Nonparametric functional regression with multiple predictors

#> =============================================================

#> Number of observations: 100

#> Number of functional predictors: 2

#> Smoother type: S.NW

#> Weights: 0.5, 0.5

#> Bandwidth: 0.2809

#> R-squared: 0.0632Mixed Functional and Scalar Predictors

Real datasets often include both functional and scalar covariates.

fregre.np.mixed() handles this by selecting separate

bandwidths for the functional and scalar parts.

# Add a scalar covariate

z <- rnorm(n)

y_mixed <- y + 0.8 * z # scalar effect added

# Fit with functional + scalar predictors

fit_mixed <- fregre.np.mixed(fd, y_mixed, scalar.covariates = z)

print(fit_mixed)

#> Nonparametric functional regression model

#> Number of observations: 100

#> Smoother type:

#> R-squared: 0.7061Testing the Linear Model Assumption

Before choosing between linear and nonparametric methods,

flm.test() tests whether the functional linear model is

adequate. If the null hypothesis (linear relationship) is not rejected,

PC and basis regression are justified; otherwise nonparametric methods

may be preferable.

# Test H0: the relationship between X(t) and Y is linear

flm_result <- flm.test(fd_train, y_train, B = 200)

print(flm_result)

#>

#> Projected Cramer-von Mises test for FLM

#>

#> data:

#> = 2073.2, p-value = 0.13A large p-value supports the linear model; a small p-value () suggests the true relationship is nonlinear and parametric methods may be misspecified.

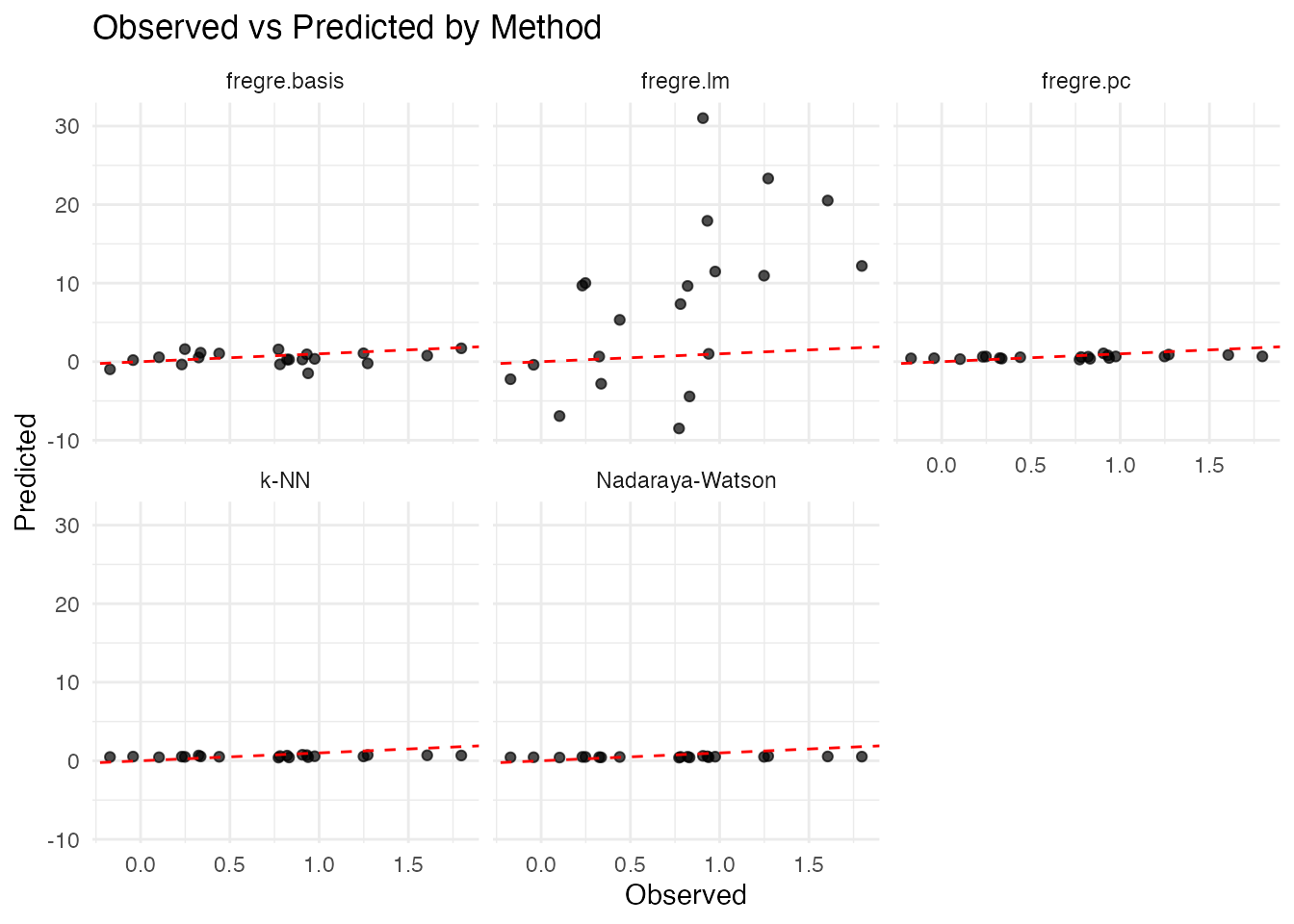

Comparing Methods

# Fit all methods on training data

fit1 <- fregre.pc(fd_train, y_train, ncomp = 3)

fit2 <- fregre.basis(fd_train, y_train, nbasis = 15)

fit3 <- fregre.np(fd_train, y_train, type.S = "S.NW")

fit4 <- fregre.np(fd_train, y_train, type.S = "kNN.gCV")

fit5 <- fregre.lm(fd_train, y_train, ncomp = 3)

# Predict on test data

pred1 <- predict(fit1, fd_test)

pred2 <- predict(fit2, fd_test)

pred3 <- predict(fit3, fd_test)

pred4 <- predict(fit4, fd_test)

pred5 <- predict(fit5, fd_test)

# Compare performance

results <- data.frame(

Method = c("fregre.pc", "fregre.basis",

"Nadaraya-Watson", "k-NN", "fregre.lm (Rust)"),

RMSE = round(c(pred.RMSE(y_test, pred1),

pred.RMSE(y_test, pred2),

pred.RMSE(y_test, pred3),

pred.RMSE(y_test, pred4),

pred.RMSE(y_test, pred5)), 4),

R2 = round(c(pred.R2(y_test, pred1),

pred.R2(y_test, pred2),

pred.R2(y_test, pred3),

pred.R2(y_test, pred4),

pred.R2(y_test, pred5)), 4),

MAE = round(c(pred.MAE(y_test, pred1),

pred.MAE(y_test, pred2),

pred.MAE(y_test, pred3),

pred.MAE(y_test, pred4),

pred.MAE(y_test, pred5)), 4)

)

knitr::kable(results, caption = "Hold-out test set performance")| Method | RMSE | R2 | MAE |

|---|---|---|---|

| fregre.pc | 0.4570 | 0.2188 | 0.3820 |

| fregre.basis | 0.8990 | -2.0226 | 0.7162 |

| Nadaraya-Watson | 0.5359 | -0.0742 | 0.4453 |

| k-NN | 0.4935 | 0.0891 | 0.4186 |

| fregre.lm (Rust) | 11.9563 | -533.6283 | 9.2836 |

Visualizing Predictions

df_pred <- data.frame(

Observed = rep(y_test, 5),

Predicted = c(pred1, pred2, pred3, pred4, pred5),

Method = rep(c("fregre.pc", "fregre.basis",

"Nadaraya-Watson", "k-NN", "fregre.lm"),

each = length(y_test))

)

ggplot(df_pred, aes(x = Observed, y = Predicted)) +

geom_point(alpha = 0.7) +

geom_abline(intercept = 0, slope = 1, linetype = "dashed", color = "red") +

facet_wrap(~ Method, nrow = 2) +

labs(title = "Observed vs Predicted by Method",

x = "Observed", y = "Predicted")

Model Diagnostics

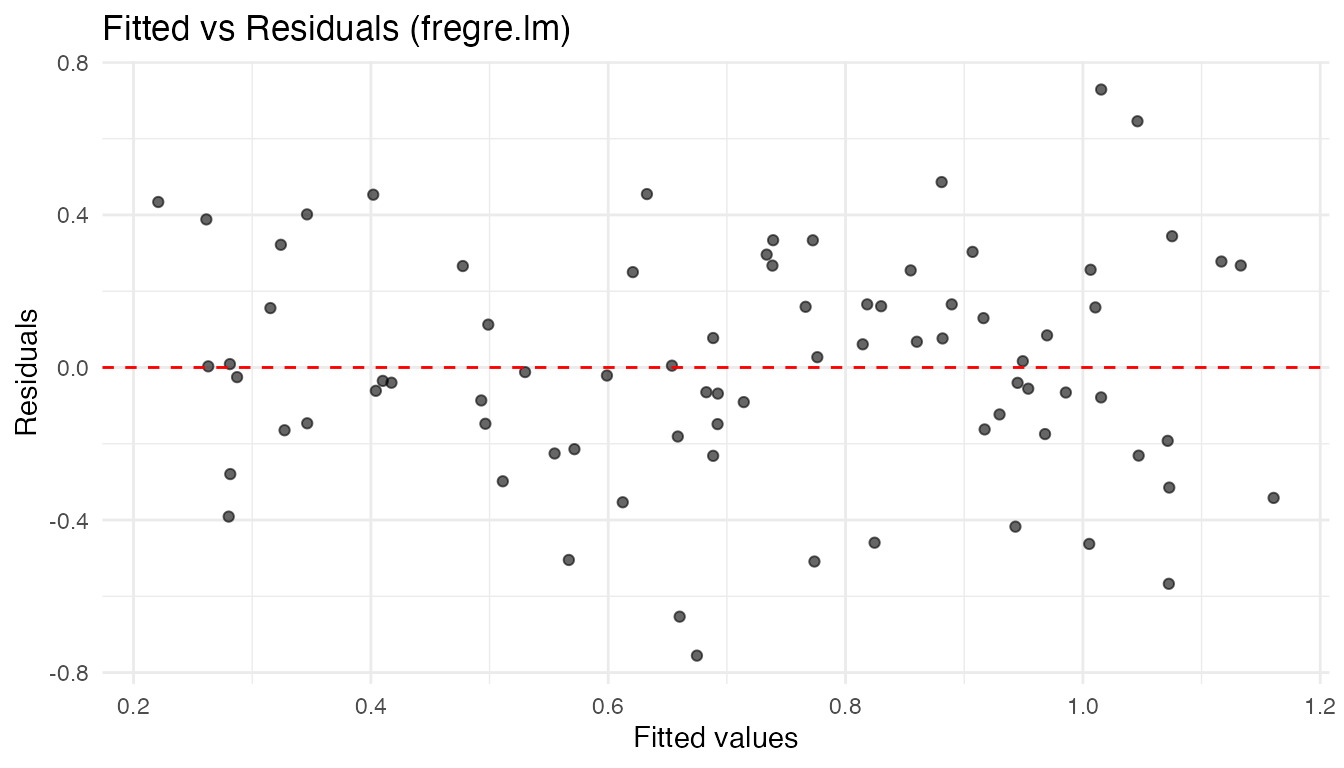

After fitting a functional linear model, standard regression diagnostics help check whether the model assumptions hold.

Residual Plots

df_diag <- data.frame(

Fitted = fit_lm$fitted.values,

Residuals = fit_lm$residuals

)

ggplot(df_diag, aes(x = Fitted, y = Residuals)) +

geom_point(alpha = 0.6) +

geom_hline(yintercept = 0, linetype = "dashed", color = "red") +

labs(title = "Fitted vs Residuals (fregre.lm)",

x = "Fitted values", y = "Residuals")

A random scatter around zero supports the linearity and constant-variance assumptions. Fan-shaped or curved patterns suggest heteroscedasticity or nonlinearity.

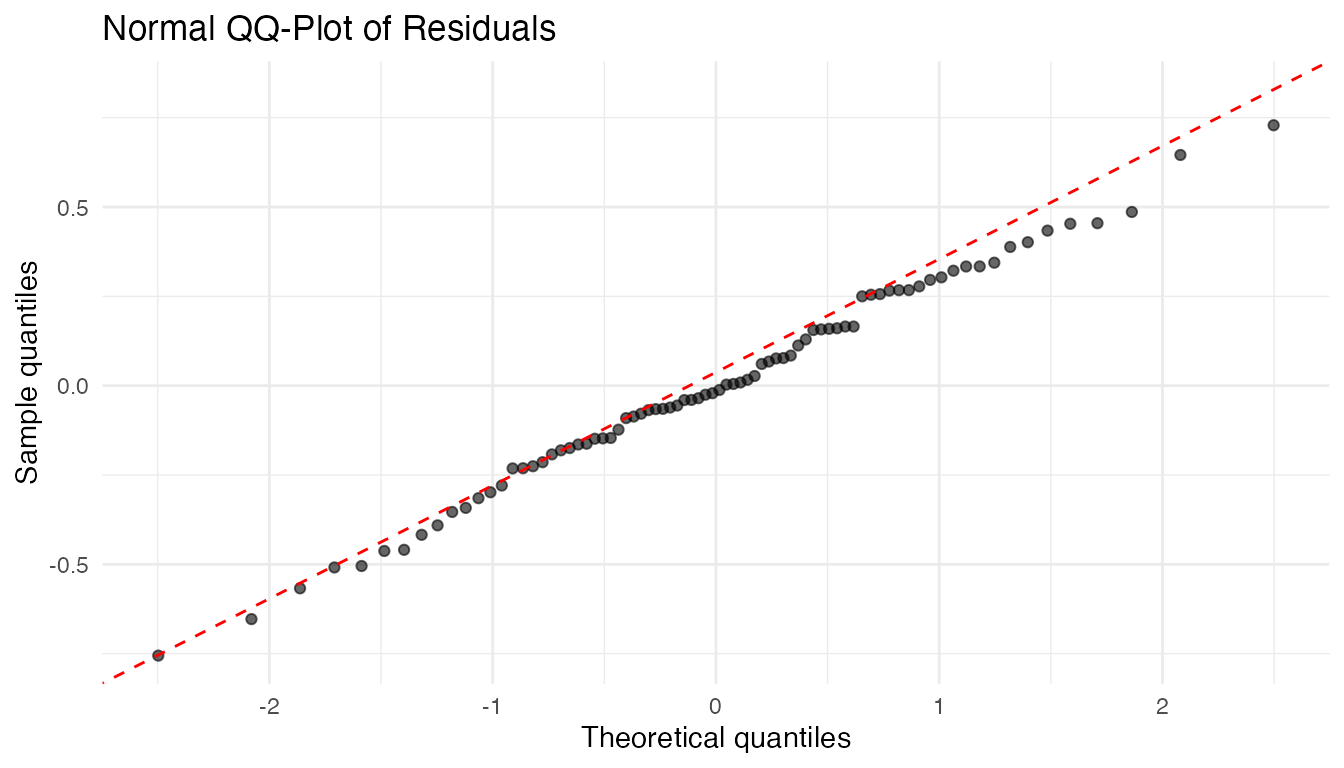

QQ-Plot of Residuals

ggplot(df_diag, aes(sample = Residuals)) +

stat_qq(alpha = 0.6) +

stat_qq_line(color = "red", linetype = "dashed") +

labs(title = "Normal QQ-Plot of Residuals",

x = "Theoretical quantiles", y = "Sample quantiles")

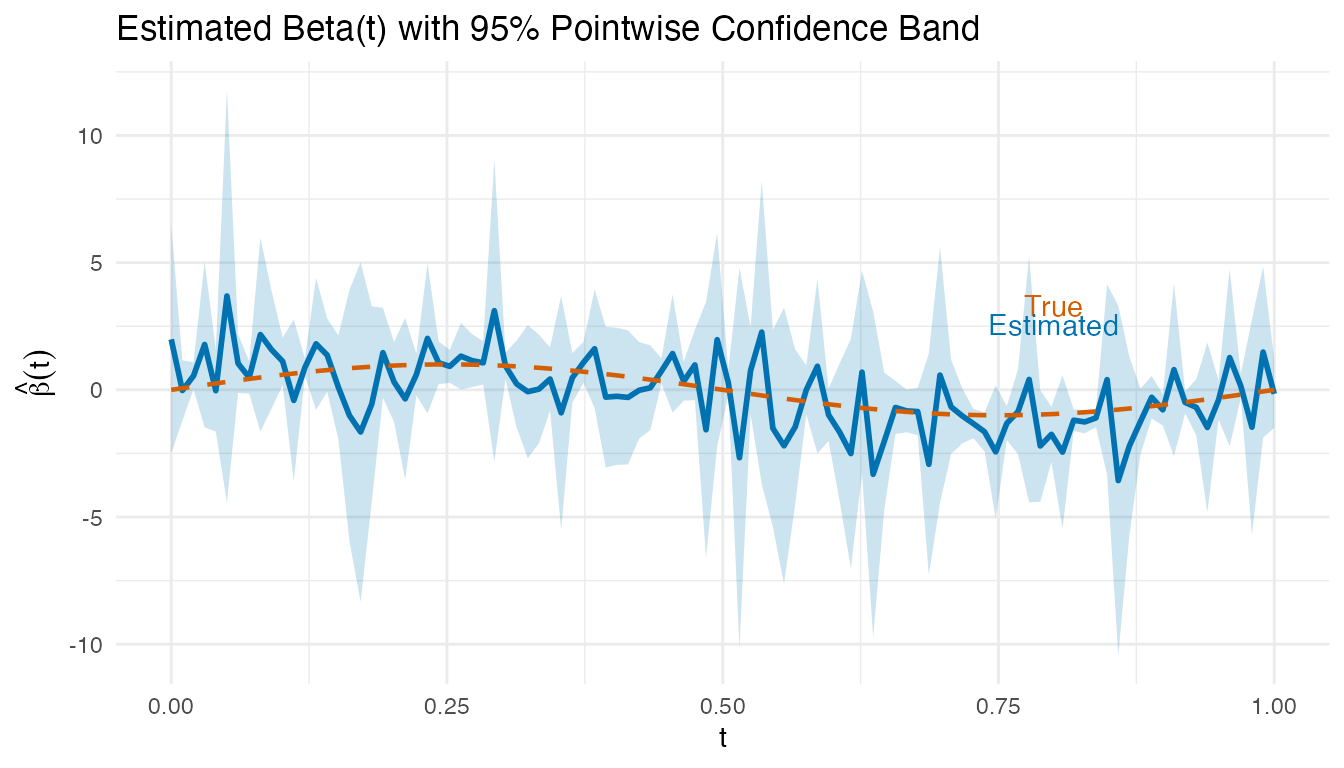

Visualizing Beta(t) with Confidence Bands

# fregre.lm stores beta(t) as an fdata object and SEs from the FPC regression

coefs <- fit_lm$coefficients[-1] # exclude intercept

loadings <- fit_lm$.fpca_rotation # m x K matrix of FPC loadings

beta_hat_lm <- as.numeric(loadings %*% coefs)

# Approximate pointwise SE via delta method using FPC score regression SEs

se_coefs <- fit_lm$std.errors[-1] # exclude intercept SE

beta_se <- sqrt(as.numeric((loadings^2) %*% (se_coefs^2)))

df_beta_ci <- data.frame(

t = t_lm,

beta = beta_hat_lm,

lower = beta_hat_lm - 1.96 * beta_se,

upper = beta_hat_lm + 1.96 * beta_se,

true_beta = beta_true_lm

)

ggplot(df_beta_ci, aes(x = t)) +

geom_ribbon(aes(ymin = lower, ymax = upper), fill = "#0072B2", alpha = 0.2) +

geom_line(aes(y = beta), color = "#0072B2", linewidth = 1) +

geom_line(aes(y = true_beta), color = "#D55E00", linetype = "dashed",

linewidth = 0.8) +

labs(title = "Estimated Beta(t) with 95% Pointwise Confidence Band",

x = "t", y = expression(hat(beta)(t))) +

annotate("text", x = 0.8, y = max(beta_hat_lm) * 0.9,

label = "True", color = "#D55E00") +

annotate("text", x = 0.8, y = max(beta_hat_lm) * 0.7,

label = "Estimated", color = "#0072B2")

Regions where the confidence band excludes zero indicate time points where the predictor significantly influences the response.

For comprehensive diagnostics (influence, Cook’s distance, DFBETAS,

etc.), see vignette("articles/regression-diagnostics").

Prediction Metrics

Model performance is evaluated using standard regression metrics:

| Metric | Formula | Interpretation |

|---|---|---|

| MAE | Average absolute error | |

| MSE | Average squared error | |

| RMSE | Error in original units | |

| Proportion of variance explained |

cat("MAE:", pred.MAE(y_test, pred1), "\n")

#> MAE: 0.3819577

cat("MSE:", pred.MSE(y_test, pred1), "\n")

#> MSE: 0.2088714

cat("RMSE:", pred.RMSE(y_test, pred1), "\n")

#> RMSE: 0.4570245

cat("R2:", pred.R2(y_test, pred1), "\n")

#> R2: 0.2188439All methods support leave-one-out cross-validation (LOOCV) for parameter selection:

This is implemented efficiently using the “hat matrix trick” for linear methods.

Practical Workflow

A recommended workflow for scalar-on-function regression:

-

Start simple: fit

fregre.lm.cv()to find the optimal number of FPC components via cross-validation. -

Check linearity: run

flm.test()on the training data. A significant p-value suggests nonlinearity. -

If linear holds: compare

fregre.lm(),fregre.pc(), andfregre.basis()— all estimate the functional linear model with different regularization strategies. -

If linearity is rejected: try

fregre.np()with bandwidth cross-validation (fregre.np.cv()). -

Evaluate: hold out a test set and compare methods

with

pred.RMSE(),pred.R2(), andpred.MAE(). - Diagnose: check residual plots and the estimated for interpretability.

set.seed(42)

tr <- sample(n, 70)

te <- setdiff(1:n, tr)

fd_tr <- fd[tr, ]

fd_te <- fd[te, ]

y_tr <- y[tr]

y_te <- y[te]

# Step 1: CV for component selection

cv <- fregre.lm.cv(fd_tr, y_tr, k.range = 1:6, nfold = 5)

# Step 2: Test linearity

linearity <- flm.test(fd_tr, y_tr, B = 200)

cat("FLM test p-value:", linearity$p.value, "\n")

#> FLM test p-value: 0.65

# Step 3-4: Fit best linear and nonparametric

fit_best_lm <- fregre.lm(fd_tr, y_tr, ncomp = cv$optimal.k)

fit_best_np <- fregre.np(fd_tr, y_tr, type.S = "kNN.gCV")

# Step 5: Evaluate

pred_lm_wf <- predict(fit_best_lm, fd_te)

pred_np_wf <- predict(fit_best_np, fd_te)

cat("Linear RMSE:", round(pred.RMSE(y_te, pred_lm_wf), 4),

"| R2:", round(pred.R2(y_te, pred_lm_wf), 4), "\n")

#> Linear RMSE: 20.2929 | R2: -1967.406

cat("Nonpar RMSE:", round(pred.RMSE(y_te, pred_np_wf), 4),

"| R2:", round(pred.R2(y_te, pred_np_wf), 4), "\n")

#> Nonpar RMSE: 0.5028 | R2: -0.2086Method Selection Guide

FPC Regression (fregre.lm /

fregre.pc):

- Best when the functional predictor has clear dominant modes of variation

- Computationally efficient for large datasets

- Interpretable: each PC represents a pattern in the data

-

fregre.lm()is the only model with full explainability support

Basis Expansion Regression

(fregre.basis):

- Best when you believe is smooth

- Use B-splines for local features, Fourier for periodic patterns

- The penalty parameter provides automatic regularization

- Good when you want to visualize and interpret

Nonparametric Regression

(fregre.np):

- Best when the relationship between and may be nonlinear

- Makes minimal assumptions about the data-generating process

- Computationally more expensive (requires distance calculations)

- May require larger sample sizes for stable estimation

See Also

-

vignette("articles/function-on-scalar")— when the response is a curve -

vignette("articles/elastic-regression")— alignment-aware regression -

vignette("articles/functional-classification")— classifying curves (includingfunctional.logistic()) -

vignette("articles/explainability")— interpretingfregre.lm()models -

vignette("articles/regression-diagnostics")— influence, Cook’s distance, VIF -

vignette("articles/uncertainty-quantification")— prediction intervals -

vignette("articles/cross-validation")— cross-validation framework -

vignette("fpca", package = "fdars")— functional principal component analysis -

vignette("basis-representation", package = "fdars")— basis function representations

References

Foundational texts:

- Ramsay, J.O. and Silverman, B.W. (2005). Functional Data Analysis, 2nd ed. Springer.

- Ferraty, F. and Vieu, P. (2006). Nonparametric Functional Data Analysis: Theory and Practice. Springer.

- Horváth, L. and Kokoszka, P. (2012). Inference for Functional Data with Applications. Springer.

Key methodological papers:

- Cardot, H., Ferraty, F., and Sarda, P. (1999). Functional Linear Model. Statistics & Probability Letters, 45(1), 11–22.

- Reiss, P.T. and Ogden, R.T. (2007). Functional Principal Component Regression and Functional Partial Least Squares. Journal of the American Statistical Association, 102(479), 984–996.

- Goldsmith, J., Bobb, J., Crainiceanu, C., Caffo, B., and Reich, D. (2011). Penalized Functional Regression. Journal of Computational and Graphical Statistics, 20(4), 830–851.

- Ferraty, F., Laksaci, A., and Vieu, P. (2006). Estimating Some Characteristics of the Conditional Distribution in Nonparametric Functional Models. Statistical Inference for Stochastic Processes, 9, 47–76.