Computes the Brownian motion (Wiener process) covariance function: $$k(s, t) = \sigma^2 \min(s, t)$$

Details

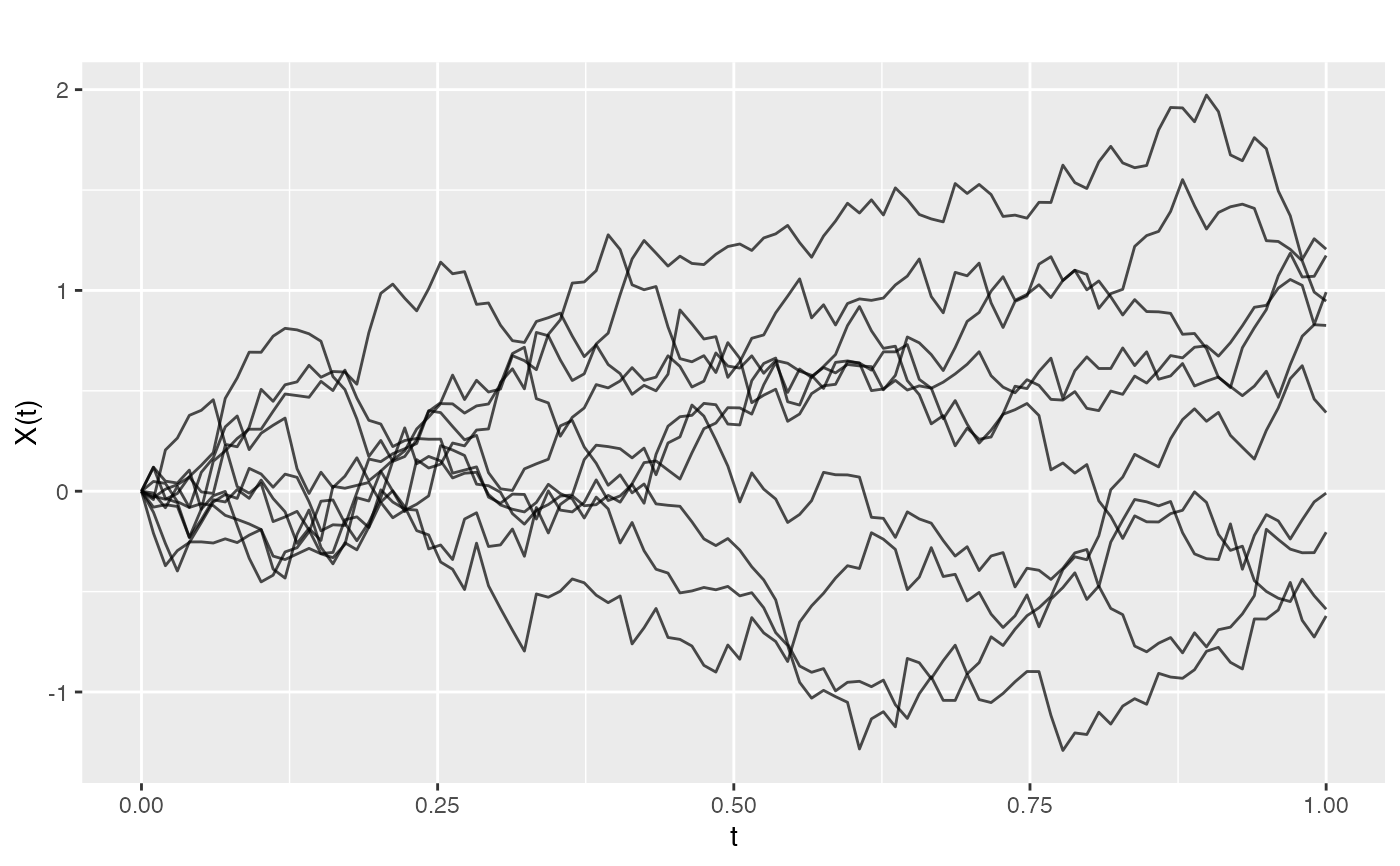

The Brownian motion covariance produces sample paths that start at 0 and have independent increments. The covariance between two points equals the variance times the minimum of their positions.

This covariance is only defined for 1D domains starting at 0.

Examples

# Generate Brownian motion paths

cov_func <- kernel.brownian(variance = 1)

t <- seq(0, 1, length.out = 100)

fd <- make.gaussian.process(n = 10, t = t, cov = cov_func)

plot(fd)