Computes the exponential covariance function: $$k(s, t) = \sigma^2 \exp\left(-\frac{|s-t|}{\ell}\right)$$

Details

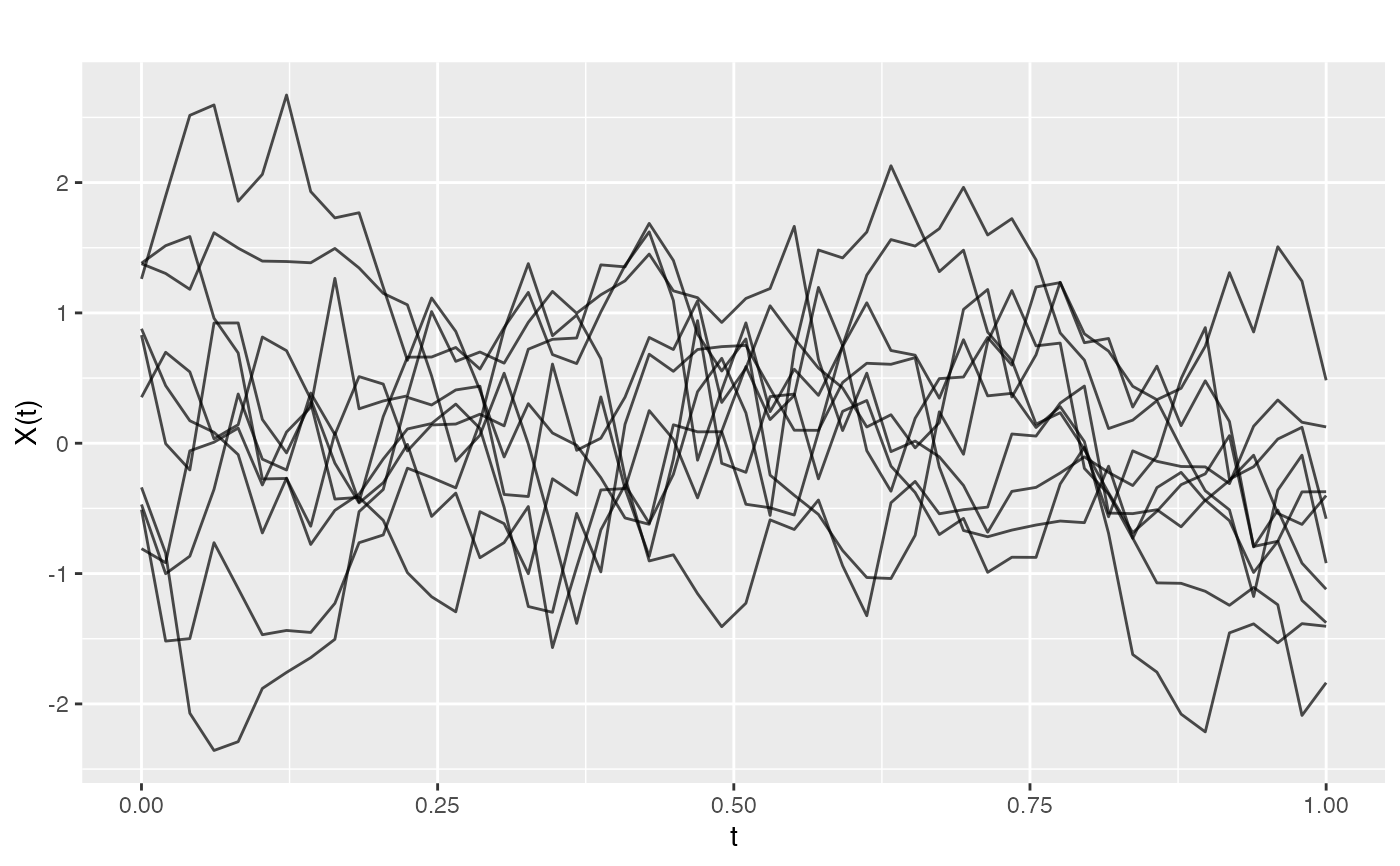

This is equivalent to the Matern covariance with \(\nu = 0.5\). Sample paths are continuous but not differentiable (rough).

The exponential covariance function produces sample paths that are continuous but nowhere differentiable, resulting in rough-looking curves. It is a special case of the Matern family with \(\nu = 0.5\).

Examples

# Create an exponential covariance function

cov_func <- kernel.exponential(variance = 1, length_scale = 0.2)

# Evaluate covariance matrix

t <- seq(0, 1, length.out = 50)

K <- cov_func(t)

# Generate rough GP samples

fd <- make.gaussian.process(n = 10, t = t, cov = cov_func)

plot(fd)